The Two Holy Cities

We concentrate on Makkah and Madinah the most within the Kingdom.

They are among the most visited places on earth and among the least served by institutional real estate capital.

They are also the most regulated and the hardest to enter.

This is exactly why focus, local knowledge, and the right structures matter. Both cities sit at the centre of long-term, faith-driven demand that does not rise and fall with market sentiment.

Destination of Faith

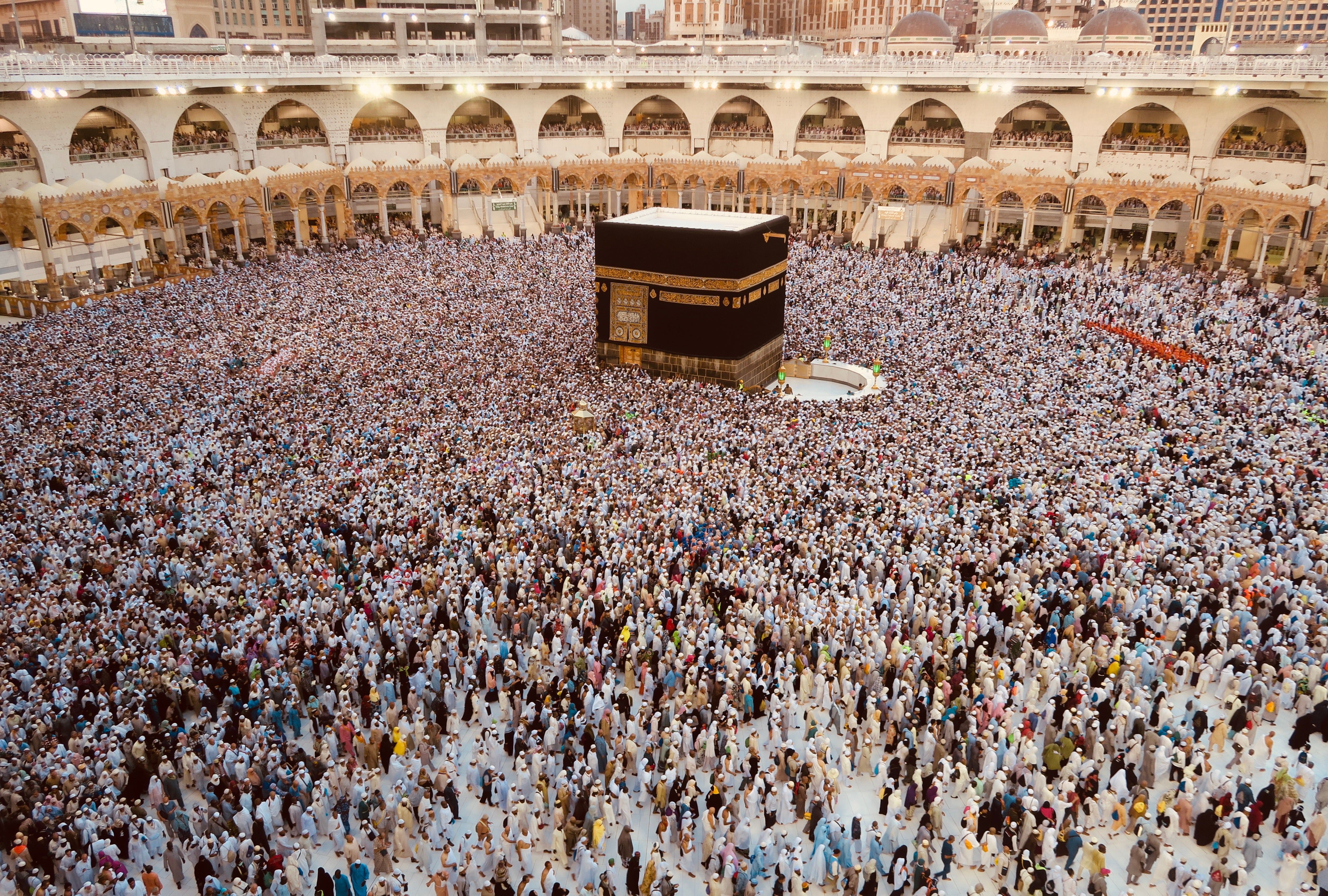

About Makkah al-Mukarramah

Makkah is the holiest city in Islam and the destination of the Hajj and Umrah pilgrimages.

It is the third most populated city in the Kingdom, with around 2.5 million residents, and it receives some 25 million overnight visitors a year.

International pilgrim numbers have risen sharply, roughly tripling over three years, and the experience itself has been transformed, with visitor satisfaction rising from around 11 percent in 2018 to about 90 percent in 2025.

The pressure on the city is most visible in hospitality. Demand for quality rooms runs well ahead of supply, with a shortfall of more than 170,000 hotel keys projected by 2030.

For us, Makkah is primarily a hospitality opportunity, approached through regulated structures and local partnerships.

Primary Focus

About al-Madinah al-Munawwarah

Madinah is our primary focus. It is the city where the gap between demand and supply is widest, across almost every category of real estate. The city records the highest hotel occupancy in the Kingdom, above 70 percent, yet its development pipeline is among the smallest relative to demand of any comparable city in the region.

The hotel room deficit is projected to reach around 70,000 keys by 2026, more than three times the gap recorded in 2024.

On the residential side, independent analysis points to a shortfall of around 73,000 homes by 2030, driven by genuine population inflow and by visitors who stay roughly ten days on average.

Madinah is one of only a small number of Saudi cities with positive demographic inflow.

Demand is also broadening beyond the area around the Prophet’s Mosque.

The city is activating more than one hundred historical and heritage sites across a thirty kilometre network, which extends how long visitors stay and widens what they need, from hotels and serviced residences to retail and food and beverage.

Independent estimates point to a gap of more than 200 food and beverage outlets serving this growing visitor base.

A recent change now allows foreign Muslims to acquire property on long leasehold, opening a new and durable source of demand.

Independent surveys of high-net-worth buyers put the average budget for premium Madinah property at around USD 4.6 million, with roughly three in ten willing to commit more than USD 5 million.

The firm’s founder has family roots in Madinah, in the Qubba neighbourhood. The city is not an abstract opportunity to us.